Introduction

Our planet is heating up rapidly and it’s a scientific fact that humanity will face disaster if we don’t cut down on greenhouse gas emissions massively and quickly. But climate change itself is not our problem. It’s merely a symptom of another problem that’s even bigger in scale and that many people don’t quite see yet. If we don’t succeed in understanding and solving this core problem (which is the root cause of many other problems as well), we won’t be able to tackle climate change either.

Climate change impacts manifest in the form of irregular changes and more severe weather patterns, leading to floods and other natural calamities. Although there is no single internationally accepted definition of vulnerability to climate change, Pakistan ranks among the top 10 most vulnerable countries in various indexes and reports. According to one assessment, Pakistan is at number eight in terms of vulnerability to climate change. The losses suffered because of climate change and its vulnerability exacerbates myriad challenges including internal security, population bulge, growing energy gap, issues with education and healthcare systems, and increasing unemployment.1

Pakistan CPEIR 2015 Key Findings:1

- Climate Change has been recognized in Pakistan as a core component of the development model required for growth, poverty reduction and wellbeing of population. This is embedded in national economic policies such as the Framework for Economic Growth (FEG) 2011, Vision 2025, and the accompanying Medium- Term Development Plan (2010–2015).

- The demand for more energy and the need to mitigate growing greenhouse gas (GHG) emissions require substantial investments of over 5% of GDP.

- The number of climate-relevant projects within each government institution varied widely across the studied years. The total federal expenditure on climate change was estimated to be in between 5.8 to 7.6% of the total public expenditures.

- In the 18th amendment of the Constitution the climate change responsibilities have been concurrently assigned to both federal and provincial governments. Mainstreaming climate change across sectors is a challenge and there is confusion on responsibilities, in terms of defining the federal and provincial mandates. In the case of provinces, the climate policy impetus is provided under the Provincial Environmental Protection Act, 2014 with the institutional remit for climate designated to the Climate Change Cell within the Environmental Protection Agency (EPA).

- Climate change is not routinely considered in the selection of development expenditures and allocations in Pakistan. As a result there is no public financial management driver for climate-sensitive budgeting for development budgets.

- The integration of climate change in the budget process requires concerted efforts from the Ministry of Finance (MoF), Ministry of Planning Development & Reform (MPDR) and Ministry of Climate Change (MCC). The development of a Climate Change Financial Framework (CCFF) can serve as the instrument to link climate change policy with budget allocations.

1Source: Pakistan Climate Change Financing Framework Oct 2017 (report published on https://www.climatefinance-developmenteffectiveness.org/sites/default/files/publication/ attach/Pakistan-CCFF-Oct-2017.pdf)

CPEIR (Climate Public Expenditure and Institutional Review)

Greenhouse Gas Emissions and its Sources

Greenhouse gases trap heat and make the planet warmer. Human activities are responsible for almost all of the increase in greenhouse gases in the atmosphere over the last 150 years. The largest source of greenhouse gas emissions from human activities in the United States is from burning fossil fuels for electricity, heat, and transportation.

Pakistan emitted 342 million metric tons (MtCO2e) in 2012 (which is 0.72% of world total), with the energy sector contributing 46 percent to overall emissions, followed by agriculture (41%), land-use change and forestry (6%), industrial processes (5%) and waste (2%). Greenhouse gas emissions increased by 87 percent from 1990 – 2012, primarily due to the energy and agriculture sector emissions. 2

Energy: The electricity and transportation subsectors were the main drivers of energy sector emissions growth, contributing 30% and 27%, respectively, of the total energy sector increase. The relative share of GHG-intensive fossil fuels (coal, oil, and natural gas) in the electricity generation mix increased from 54% in 1990 to 64% in 2012. The total amount of electricity consumption also doubled during this time, from 31 billion kWh in 1990 to 77 billion kWh in 2012, driven by improved access to electricity, from 60% of the population in 1990 to 94% in 2012. The number of motor (private) vehicles registered increased from 2 million vehicles in 1992 to more than 9 million vehicles registered in 2011, driving an increase in consumption of fuel oil and compressed natural gas in the transport sector. 2

Agriculture: 54% of emissions growth from this sector is due to enteric fermentation while another 18% came from synthetic fertilizers and 14% came from manure left on pasture. These trends are accompanied by growth of the livestock population, which increased at an annual growth rate of 2.4% between 1990 and 2000, and approximately 3.5% between 2001 and 2011. The largest sector of Pakistan’s economy, agriculture contributes about 24% of the Gross Domestic Product (GDP). 2

2 Source: GHG Emissions Fact Sheet Pakistan https://www.climatelinks.org/sites/default/files/asset/docume nt/GHG%20Emissions%20Fact%20Sheet%20Pakistan_6-3- 2016_edited_rev%2008-18-2016.pdf

Climate baseline and climate future

Vulnerability, Risk Reduction, and Adaptation to Climate Change published by World Bank in April 20113, following are the priority adaptation projects:

- Water management and planning for the Indus

- Adjusting cropping patterns and type with water availability

- Fodder banks/improved feeding to help restore degraded lands

- Monitoring coastal zones in order to protect biodiversity

Below is the climate baseline summary for Pakistan (since 1960) 3

- Mean rainfall in the arid plains of Pakistan and the coastal belt has decreased by 10-15%.

- Over the same period mean rainfall in Northern Pakistan has increased.

- The number of hot days has increased by 20 days.

- The number of hot nights has increased by 23 days.

- The number of cold nights has decreased by 9.7 days.

- The number of heavy rainfall events has increased, and the nine heaviest rains recorded in 24 hours were recorded in 2010.

SpringerLink published in December 2019 4

That the devastations and damages caused by climate change are apparent across the globe, specifically in the South Asian region where vulnerabilities to climate change among residents are high and climate change adaptation and mitigation awareness are extremely low. Pakistan’s low adaptive capacity due to high poverty rate, limited financial resources and shortage of physical resources, and continual extreme climatic events including varying temperature, continual flooding, melting glaciers, saturation of lakes, earthquakes, hurricanes, storms, avalanches, droughts, scarcity of water, pest diseases, human healthcare issues, and seasonal and lifestyle changes have persistently threatened the ecosystem, biodiversity, human communities, animal habitations, forests, lands, and oceans with a potential to cause further damages in the future. The likely effect of climate change on common residents of Pakistan with comparison to the world and their per capita impact of climate change are terribly high with local animal species such as lions, vultures, dolphins, and tortoise facing extinction regardless of generating and contributing diminutively to global Greenhouse Gas (GHG) emissions. The findings of the review suggested that GHG emissions cause climate change which has impacted agriculture livestock and forestry, weather trends and patterns, food water and energy security, and society of Pakistan. This review is a sectorial evaluation of climate change mitigation and adaption approaches in Pakistan in the aforementioned sectors and its economic costs which were identified to be between 7 to 14 billion USD per annum. The research suggested that governmental interference is essential for sustainable development of the country through strict accountability of resources and regulation implemented in the past for generating state-of-the-art climate policy.

3 Source: Climate Risk and Adaptation Country Profile https://climateknowledgeportal.worldbank.org/sites/default/fil es/2018-10/wb_gfdrr_climate_change_country_profile_for_P AK.pdf

4 Source: SpringerLink (a web portal facilitates scientific research)

https://link.springer.com/article/10.1007/s10661-019-7956-4#

:~:text=The%20effects%20of%20climate%20change%20in% 20Pakistan%20are%20highly%20severe,heat%20waves%2 C%20saturation%20of%20lakes%2C

Task Force on Climate-Related Financial Disclosure

The Financial Stability Board created the Task Force on Climate-related Financial Disclosures (TCFD) to improve and increase reporting of climate-related financial information. In June 20175, TCFD published final report which includes the TCFD recommendations on climate-related financial disclosures are widely adoptable and applicable to organizations across sectors and jurisdictions. They are designed to solicit decision-useful, forward-looking information that can be included in mainstream financial filings. The recommendations are structured around four thematic areas that represent core elements of how organizations operate: governance, strategy, risk management, and metrics and targets.

TCFD Recommendations and Supporting Recommended Disclosures are mentioned below:

Governance – Disclose the organization’s governance around climate related risks and opportunities.

- Describe the board’s oversight of climate-related risks and opportunities.

- Describe management’s role in assessing and managing climate-related risks and opportunities.

Strategy – Disclose the actual and potential impacts of climate-related risks and opportunities on the organization’s businesses, strategy, and financial planning where such information is material.

- Describe the climate-related risks and opportunities the organization has identified over the short, medium, and long term.

- Describe the impact of climate related risks and opportunities on the organization’s businesses, strategy, and financial planning.

- Describe the resilience of the organization’s strategy, taking into consideration different climate-related scenarios, including a 2°C or lower scenario.

Risk Management – Disclose how the organization identifies, assesses, and manages climate-related risks.

- Describe the organization’s processes for identifying and assessing climate-related risks.

- Describe the organization’s processes for managing climate-related risks.

- Describe how processes for identifying, assessing, and managing climate-related risks are integrated into the organization’s overall risk management.

Metrics and Targets – Disclose the metrics and targets used to assess and manage relevant climate-related risks and opportunities where such information is material.

- Disclose the metrics used by the organization to assess climate related risks and opportunities in line with its strategy and risk management process.

- Disclose Scope 1, Scope 2, and, if appropriate, Scope 3 greenhouse gas (GHG) emissions, and the related risks.

- Describe the targets used by the organization to manage climate-related risks and opportunities and performance against targets.

Scope 1 refers to all direct GHG emissions.

Scope 2 refers to indirect GHG emissions from consumption of purchased electricity, heat, or steam.

Scope 3 refers to other indirect emissions not covered in Scope 2 that occur in the value chain of the reporting company, including both upstream and downstream emissions.

5 Source: TCFD – Final Report https://assets.bbhub.io/company/sites/60/2020/10/FINAL-20 17-TCFD-Report-11052018.pdf

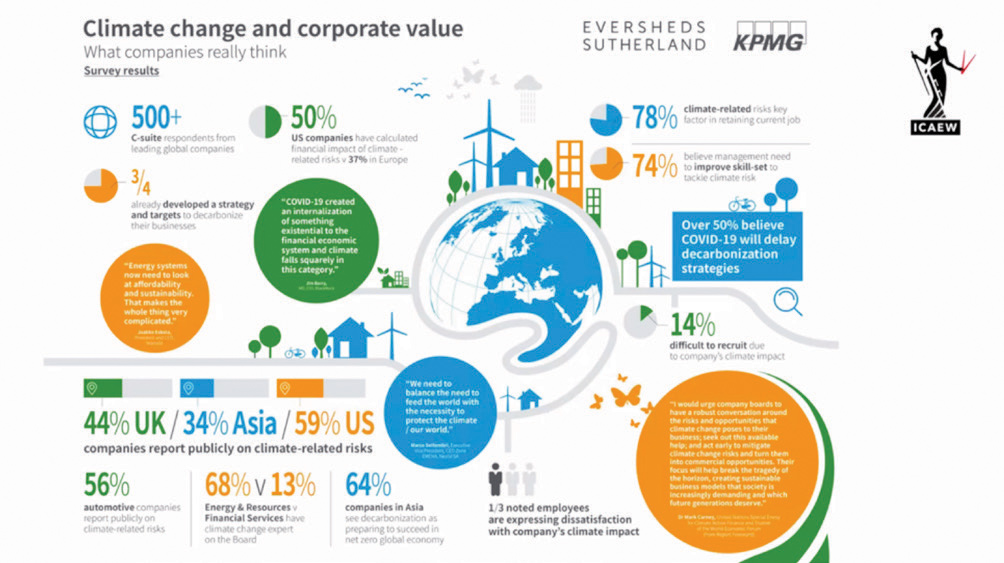

ICAEW shared to its member a survey result:

Conclusion

Climate change is not a problem of one country or specific industries. It is a combined responsibility for all stakeholders including general public and professionals to play their part in restoring the environment of the society for our future generations.

{kind=link}

{kind=link}

{kind=link}