How businesses can respond during Covid-19

Loading the Elevenlabs Text to Speech AudioNative Player...

By STELLA LAU

The coronavirus disease (Covid-19) has infected people in 216 countries and territories, sent stock markets crashing to new lows, caused unemployment to spike to record highs, and is likely to send many advanced economies into recession this year. The International Monetary Fund (IMF) calls it the “worst recession since the Great Depression”. Apart from the health emergency, extreme but necessary measures from closing borders to shutting down businesses have plunged many countries into deep economic crisis and uncertainty. In its April world economic outlook, IMF had projected a global growth in 2020 to fall to -3%, a downward revision by a substantial 6.3 percentage points from its January forecast.

Not only is Covid-19 harder hitting than the Severe Acute Respiratory Syndrome or SARS in 2003, it is likely to be more prolonged. With a global recession looming, businesses are faced with a marathon of challenges. Beyond the performance of their domestic economies, they will be affected by international demand that has nosedived and disrupted supply chains. In a highly interconnected world, countries cannot fully recover as other nations continue to struggle to cope with the virus. Overall recovery will take time. Even in an optimistic scenario that the pandemic fades in the second half of 2020, IMF expects any economic recovery in 2021 to only be “partial”.

Apart from responding to immediate challenges, businesses must plan for an extended difficult period ahead, at least beyond a year. Scenario planning can help businesses spot possible pitfalls so that rational and preventative steps can be taken to mitigate any uncertainty. Action plans can include defensive strategies such as cost cutting and retaining existing customers, as well as offensive strategies such as selling online and innovating product and service offerings.

ADDRESSING LIQUIDITY FIRST AND FOREMOST

The immediate challenge for businesses is to ensure survival. Managing cash flow and conserving cash to maintain liquidity will be key.

First, to have clarity on the current status, businesses must keep a close eye on their cash flow and position through monitoring working capital needs and updating cash flow forecasts regularly. Accountancy and finance professionals should flag any warning signs such as deviations between actual and forecasted cash flows, and investigate these deviations to improve accuracy in future projections. In addition, with their relevant skill sets, they are well-equipped to play a central role in helping their employers manage cash flows in a crisis. We map out a three-pronged approach that businesses can use as a guide, namely,

- conserve

- access financing support

- worst-case planning

This approach is adapted from a Deloitte white paper on managing cash flow during a period of crisis.

A) Conserve

One of the first things is to reprioritise expenditures so that money is spent only on items which are absolutely necessary to support or grow the business. This entails analysing the cost structure of the business, and was discussed in the article, “Implications Of Covid-19 On Businesses”, published in the May issue of the IS Chartered Accountant Journal. In a nutshell, cost structures are expected to change with Covid-19. Some costs will necessarily increase to address certain issues. Hence, it is important for businesses to know where they should spend their every single dollar.

Having said that, businesses can still explore cost-cutting measures. A quick way is to reduce variable costs such as imposing a hiring freeze and restricting discretionary spend on travel, entertainment and training. Before resorting to laying off employees, businesses should consider longer-term benefits of retaining existing employees for the rebound, and first explore other options such as redistributing outsourced or contract work to permanent employees.

Secondly, businesses can revisit their capital investments. Identify investments that can be postponed or reconsidered. Also, review investment plans, to better position for recovery, that can help the company establish a competitive advantage.

Conserving resources also lies in good inventory management. The key is to strike the right balance between having enough inventory to sustain production needs and order fulfilment, and ensuring cash flow from sale of finished goods inventory. Making significant cuts to inventory levels may seem the most obvious solution but could backfire to severely impact production and customer service. Therefore, it is critical that businesses know which of their products are more in demand vis-à-vis those which are less popular, to help in their inventory management. Another way to better manage this is to increase visibility of the supply chain, which will enable better planning and enhance inventory management. This will be further discussed later in this article.

Lastly, as far as possible, businesses should collect receivables that are due. This is the most direct way of bringing liquidity back into the system. Businesses can consider leveraging good working relationships to request for timely payments to meet immediate cash needs. Accountancy and finance professionals can forecast cash collections based on sales projections to help their businesses quantify available cash on hand. To further help the business gain better visibility of its cash flow position, they can put in place controls to prioritise payments and establish real-time reporting of key metrics.

B) Access financing support

The next important thing to do is to map out available financing options such as emergency credit lines and overdraft facilities with banks. Businesses should also tap into available subsidies and financing support from the government. Singapore businesses can benefit from schemes announced in the four Singapore Budget 2020 packages, such as the Temporary Bridging Loan Programme, the Enterprise Financing Scheme (EFS)–SME Working Capital Loan, and the EFS–Trade Loan. However, businesses should take note of the eligibility conditions which apply for these schemes.

For example, the Jobs Support Scheme (JSS) requires that employers do not retrench employees or put them on no-pay-leave to be entitled to the JSS payout. For an overview of the support measures, please refer to “ISCA Covid-19 Navigator”, which was published in the May issue of this IS Chartered Accountant Journal; the Navigator is also available on the ISCA website. Finally, businesses may wish to claim business interruption insurance if these policies are in place. Accountancy and finance professionals can help to evaluate and advise on the different financing options available if their employers wish to go down this route.

C) Worst-case scenario planning

In the worst-case scenario where various efforts to generate liquidity have proven futile, such as when clients are not paying or are in trouble, businesses may be forced to resort to worst-case options. This can include cutting fixed costs and downsizing the business to raise funds. Businesses can explore entering into partnerships to enhance their attractiveness to investors. Even though it may seem pessimistic, it is worthwhile to plan for less favourable scenarios, so that the business can stay focused on a rational course of action and do its best to turn things around.

SCENARIO PLANNING

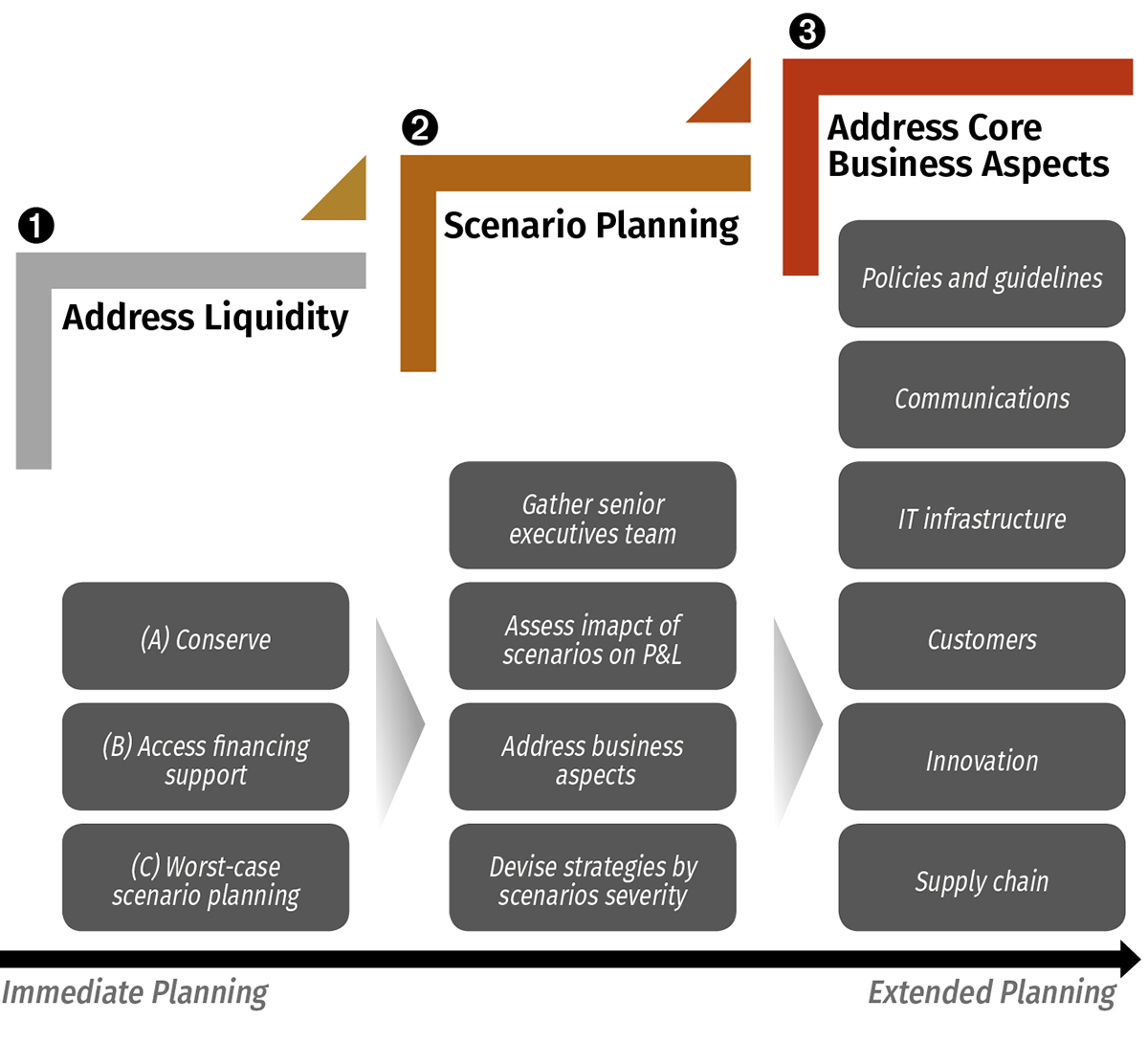

Once there is some assurance of liquidity and business viability, it is essential to expand on scenario planning. This is the time to fight a winning war.

First, businesses should gather a team of senior executives to assess the impact of various scenarios and risk factors on the profit and loss account, across revenue, cost, cash and operations. Then, establish a framework of all the business aspects to be addressed. Against each aspect, they should outline best practices and devise strategies relevant to varying levels of severity of scenarios.

In general, there are core business aspects that businesses will need to address with importance, as laid out in the next section. Figure 1 summarises a business response plan and checklist that businesses can use to change or adapt to the evolving circumstances during these challenging times.

Figure 1 Summary – Business Response Framework to Covid-19

CORE BUSINESS ASPECTS TO ADDRESS

CORE BUSINESS ASPECTS TO ADDRESS

1) Policies and guidelines

As the coronavirus is highly contagious, the priority must be to protect the health and safety of employees by implementing organisation-wide policies and arrangements. According to a survey by global professional services firm Aon released on 13 May 2020, protecting “health, safety and welfare” of employees as work resumes was the top priority for nine out of 10 businesses surveyed in Singapore. It is important for businesses to make well-considered decisions focused on their people, apart from being concerned with the balance sheets, as this also shapes the future of their organisations.

As cases of local community transmission have been coming down in Singapore, restrictions will be gradually relaxed so that economic activities can resume. However, it is still necessary to put in place measures at the workplace to provide a safe working environment and prevent the reemergence of community infections.

To resume operations, all businesses should implement safe management measures at the workplace. Details on these measures have been issued by the tripartite partners comprising Ministry of Manpower (MOM), National Trades Union Congress (NTUC) and Singapore National Employers Federation (SNEF).

Businesses should communicate and explain these measures to employees prior to resuming work, and put up signs where necessary to ensure strict adherence. Businesses should also keep in mind that these measures must be implemented in a sustainable manner for as long as necessary. The following is an extract of official requirements for safe management measures at the workplace:

- Reduce physical interaction and ensure safe distancing at workplaces. For example, implement telecommuting and conduct meetings virtually where possible. Employers must also cancel and defer all events or activities that involve close and prolonged contact among participants, for example, conferences, seminars, exhibitions and social gatherings and interactions.

- For job roles or functions where employees cannot work from home, stagger working and break hours or implement shift or split team arrangements.

- When physical interaction is required at the workplace, always ensure at least one-metre physical distance between persons.

- Support contact tracing requirements. For example, employers should encourage all employees to download and activate the TraceTogether app.

- Employers must limit access to the workplace to only essential employees and authorised visitors.

- Require use of personal protective equipment (example, masks) and observe good personal hygiene, such as washing hands regularly and refraining from touching the face.

- Ensure cleanliness of workplace premises by stepping up the cleaning of workplace premises.

- Implement health checks and protocols such as regular temperature screening and declarations for all onsite employees and visitors.

- Adhere to travel advisories from the Ministry of Health (MOH). At the time of writing this article in mid-May, Singaporeans are advised to defer all travel abroad. Businesses should refer to the MOH website for the latest updates.

- Have a plan for unwell cases. For example, employees feeling unwell must report to the employer, leave the workplace and consult a doctor immediately.

- Have a followup plan to manage confirmed cases, including vacating and cordoning off the section of the workplace where the confirmed case worked, and carrying out thorough cleaning and disinfecting.

For more details, please refer to MOM’s Covid-19 Advisory: Requirements For Safe Management Measures At The Workplace After Circuit Breaker Period.

2) Communications

With clear policies laid out, it is also vital to have a sound internal communications plan. Communicating changes in policies and guidelines and explaining how and why decisions are made, so that employees understand what is going on, is important for adherence and implementation.

Furthermore, keeping employees informed of the ongoing situation in a timely and open manner establishes an official source of reliable information within the organisation, and trust that management is acting on the necessary. This can reduce uncertainty and anxiety overall.

As work norms are changing, such as with telecommuting, businesses should share tips and resources to ease employees into these changes. They should maintain open communication channels between management and team members to align and adjust to changes in work expectations and build mutual understanding. It is important to keep morale up, assure employees that their welfare is taken care of and address any concerns.

There should also be communications to shareholders on the financial position and priorities of the business. This can also include the financial impact and resultant changes to earlier earnings projections, as well as action plans to mitigate risks. Such communication during a time of uncertainty can be extremely valuable. Informing shareholders of the planned next steps to cope with the current situation provides assurance and retains confidence.

In addition, businesses should also establish communications with customers to keep them updated on the status of the operations especially if this will impact them. This is further explained in the “Customers” section below.

3) IT infrastructure

An extended period on telecommuting can strain remote connectivity networks due to higher traffic. Enhancing IT infrastructure, both hardware and software, to boost remote connectivity and facilitate access to shared databases, and communication and virtual meeting apps can minimise disruption to business activity and productivity.

More crucially, businesses must not lose sight of cybersecurity risks. Recently, a live stream of a geography lesson to a group of students in Singapore on video-conferencing platform Zoom was hacked with obscene pictures, reflecting the risk of the online platform. Hackers can cripple any business, and stepping up on cybersecurity and prevention of data breaches must be high on the agenda of management personnel.

In Singapore, the government has listed certain sectors or areas as essential services that remain accessible to the public and businessesduring the circuit breaker period. In the area of information and communications, these include ICT (information and communications technology) and support tools, software and services for businesses and individuals to enable telecommuting, video-conferencing, e-commerce, finance, enterprise networks/systems and IT (information technology) services. Cybersecurity services in support of other essential services and the digital economy are also listed as essential services. Even if the circuit breaker is switched on again in the near future, businesses should be able to find vendors who can help them enhance their IT infrastructure. They can also approach the Infocomm Media Development Authority and SGTech which have curated resources, including digital solutions, grants and training courses, that businesses can tap on to help them during such trying times.

4) Customers

Customers are the lifeblood of business. Businesses must protect their relationships with customers. Looking out for one another in difficult times strengthens relationships. Hence, businesses should continue engaging their customers. For example, in a business-to-business (B2B) setting, informing corporate clients of any delays in order fulfilment will greatly aid their inventory management and production planning. This is particularly important for non-essential businesses which have been required to stop operations during the circuit breaker (if it is reactivated) and no longer be able to fulfil orders. Their customers will need to be informed of the disruptions accordingly and in a timely manner, if possible.

Also, businesses can exercise more flexibility with customers, such as by not imposing minimum order requirements or accommodating requests to change delivery dates. Maintaining service standards even in difficult times by providing cancellation refunds or offering goodwill gestures to support customers’ end needs can be a major differentiation that makes companies stand out from their competitors. For example, confectionaries that were closed on short notice due to tightened circuit breaker measures can provide refunds to customers who had placed advance orders, and put up cake recipes on their websites so that customers can try them at home.

Businesses should train frontline service staff to deliver consistent treatment, so customers are not hung out to dry and left to their own devices.

For businesses that have the additional means to help, showing solidarity in crisis situations by offering free services can be advantageous for brand reputation and visibility. For example, Singtel is offering a care package of free entertainment to business solutions for SMEs.

5) Innovation

Other than defensive strategies, businesses need to consider going on the offensive. During hard times, businesses must be prepared to go the extra mile or think out of the box to find new sources of revenue. For instance, focus on higher-value customers who may still retain a higher propensity to spend, and reward them for their loyalty, such as offering loyalty discounts or freebies.

Businesses can also explore expanding service offerings to generate new revenue streams. For example, taxi and private car hirers were redirected to deliver food and groceries due to the reduction in demand for passenger service.

Establishing an online presence in the current outbreak, with restrictions on movements and social distancing, will also be instrumental to access domestic demand and possibly even overseas demand. Many businesses in Singapore had to ramp up their e-commerce presence quickly; some even had to set up one immediately (albeit a simple e-storefront) before the circuit breaker kicked in, changing their traditional brick-and-mortar businesses to adapt to changes in the environment. This is especially important for non-essential businesses which had to close their physical stores during the circuit breaker. In the first article of this series, it was shared that the government is providing strong support to help businesses digitalise. For instance, Enterprise Singapore (ESG) launched a scheme to subsidise up to 90% of the costs of selling online.

6) Supply chain

Due to the coronavirus, more than nine out of 10 Fortune 1000 companies had reported a disruption in their supply chains. To mitigate the impact and manage risks, businesses need to review their supply chain and restrategise. Here are extracted highlights of KPMG’s recommendations for businesses to assess supplier risks:

- Establish a team to focus on supply chain assessment and risk management. This team can work to reconfigure global and regional supply chain flows where possible, utilising alternative modes of transportation and conducting tradeoffs according to needs, cost, service and risk scenario analysis of all viable options.

- Map criticality of sourced materials to high-value products and revenue streams. Identify the components and raw materials that have the highest impact on revenue streams, and help to ensure scarce capacity is allocated wisely.

- Determine exposure by identifying current and buffer inventory, building tier transparency and short-term action plans.

- Conduct a value chain assessment of other risk factors that may escalate costs (example, transportation shortages may increase cost as transport companies see an opportunity to raise margins) and impact service and inventory capabilities. Take proactive action to address anticipated shortages, such as possibly pre-booking freight.

CONCLUSION

Despite the bleak current situation, businesses are not sitting ducks. In this rapidly intensifying setting, speed is of the essence. Businesses must make full use of resources and access financing support from government schemes while deploying resources strategically – being clear of must-haves and good-to-haves. To stand a better chance of withstanding the blows from Covid-19, businesses must act quickly, now.

Stella Lau is Manager, Insights & Publications, Institute of Singapore Chartered Accountants.

This article was first published by ISCA Journal. You can read the original version here.

{kind=link}

{kind=link}

{kind=link}