Singapore’s restructuring and insolvency landscape

Loading the Elevenlabs Text to Speech AudioNative Player...

By ANGELA EE

IMPENDING CHANGES AND IMPLICATIONS

The new Singapore Insolvency, Restructuring and Dissolution Act 2018 (IRDA) was passed by the Singapore Parliament on 1 October 2018 but has yet to come into force. What are some of the key changes and the implications for corporates who wish to restructure their debts, particularly against the backdrop of Covid-19 and the consequential economic repercussions?

THE LEGAL REGIME

The restructuring and insolvency regime in Singapore, which was historically modelled on English law, had undergone various amendments to streamline its laws. Introduced as the final phase, IRDA aims to further modernise and strengthen the legislation relating to debt restructurings, and to position Singapore as an international hub for cross-border debt restructuring.

In a nutshell, IRDA consolidates the personal and corporate laws relating to insolvencies and restructuring into a single statute, and incorporates concepts imported from Chapter 11 of the US Bankruptcy Code and adoption of UNCITRAL Model Law on cross-border insolvency.

Together, the key amendments increase Singapore’s attractiveness as a venue for cross-border restructuring by including provisions relating to debtor-in-possession rescue financing, a cross-class “cram down” mechanism and a worldwide stay on proceedings, not only for Singapore-incorporated debtors but also foreign debtors.

IMPLICATIONS OF SELECTED KEY AMENDMENTS

The key amendments are summarised below:

1) Enhanced schemes of arrangement

a) Automatic moratorium

Upon the filing by a debtor of an application under section 211B of the Companies Act (section 64 of IRDA), (with demonstration of, inter alia, creditor support), an automatic 30-day moratorium is granted, which restrains parties from commencement and continuation of any proceedings against the debtor. This moratorium may be extended by the Court. Courts can also order the moratorium to have extraterritorial effect. The moratorium provides much needed breathing space for debtors to engage in rehabilitative efforts.

b) “Super priority” rescue financing

An order can be granted for rescue financing to be afforded super priority over, inter alia, statutorily preferred creditors, provided that reasonable efforts were made to secure rescue financing without super priority. If certain requirements are met, it is also possible for the rescue financier to be given priority security interest over assets that are not subject to existing security interests, a subordinate security interest in property that is subjected to an existing security interest or in certain circumstances, equal or higher priority to existing security interests. This amendment is especially helpful for vulnerable companies that are already in financial difficulty and unable to otherwise secure new funding that would be critical to providing a lifeline for its survival.

c) Cross-class “cram down”

This allows the Court to approve a scheme where there are multiple classes of creditors and the requisite majorities of at least one class of creditors have voted in favour of the scheme, in circumstances where one or more classes have not done so. The Court has to be satisfied that the scheme does not unfairly discriminate between classes and is fair and equitable to each dissenting class and that overall, a majority in number of all the creditors holding three quarters of the value of the debt approved the scheme. These provisions prevent a minority dissenting class of creditors from unreasonably frustrating a restructuring that benefits creditors as a whole.

d) Pre-packaged (pre-pack) schemes

The Court has the power to approve schemes without a meeting of creditors being called. In such an instance, a pre-pack plan will be negotiated between the debtor and its creditors, before presentation to the Court. The core benefit of using a pre-pack plan is that a number of requisite formal hearings can be skipped, offering considerable time and cost savings for the company in distress.

2) Increased accessibility for foreign companies

Historically, there was some uncertainty whether foreign companies could restructure their debts in Singapore, and whether it was sufficient if the company’s centre of main interests (COMI) is in Singapore. Foreign companies can now avail themselves to restructuring options in Singapore as long as a “substantial connection” to Singapore can be demonstrated. This can be achieved by, inter alia, having the COMI in Singapore, conducting some business in Singapore, having substantial assets in Singapore, being registered in Singapore as a foreign company, or even having Singapore law as the governing law for its loan documents. This gives companies in foreign jurisdictions the option of conducting their restructuring in Singapore, where the restructuring laws are more developed, and the outcome less uncertain.

3) Restricting the operation of ipso facto clauses (not yet in force)

An ipso facto clause allows one party to terminate a contract upon the occurrence of an insolvency-related event. A new provision in IRDA restricts the ability of parties to terminate or claim an accelerated payment or forfeiture of the term under any agreement with the company by reason only that specified proceedings (for instance, for a scheme of arrangement or judicial management) have commenced in respect of the company or that the company is insolvent. It should be highlighted that parties are not precluded from exercising their contractual rights on other grounds such as non-performance by the company. This provision aims to preserve the business of the corporate and hence its value.

4) Directors’ duties: introduction of wrongful trading

A key provision in IRDA that should be highlighted is the new “wrongful trading” provision. Under the existing insolvent trading regime, civil liability for insolvent trading only arises where there has been a criminal conviction. As such, insolvent trading liability was seldom pursued historically.

Under the new provision, a company is deemed to trade wrongfully if it incurs debt or liabilities when insolvent (or becomes insolvent as a result of incurring such debt or liability), without reasonable prospect of meeting them in full. There is no longer a requirement for a criminal conviction before one may be liable for wrongful trading. This would result in a big shift in terms of directors’ duties and potential liabilities and as such, would urge directors of distressed companies to pay close attention to this new provision once it is in force.

GLOBAL UNCERTAINTIES, CHALLENGING ECONOMIC OUTLOOK AMID THE COVID-19 PANDEMIC: WHAT DOES THIS MEAN FOR STAKEHOLDERS AND COMPANIES FACING DIFFICULTIES?

The present climate which companies are operating in continues to be extremely challenging. With the global economy almost at a standstill as a result of the Covid-19 outbreak, even when lockdowns in various countries ease and businesses commence operations again, how long will it take for companies to get back to their pre-pandemic level of operations?

On 7 April 2020, the Singapore Parliament passed the Covid-19 (Temporary Measures) Act, which is aimed at providing protection from winding-up applications for companies unable to fulfil certain contractual obligations due to Covid-19, giving these companies an opportunity to “trade out” of their financial difficulties. Notably, the reliefs afforded included increasing the thresholds for insolvency from S$10,000 to S$100,000, and increasing statutory demand time limits from 21 days to six months. The interim reliefs will apply for an initial period of six months (till 19 October 2020), unless extended. It should be noted that the reliefs do not stop liabilities from accruing, nor absolve companies of their debt obligations. What can be done to prepare companies for the time when the interim reprieve is lifted and a wall of debt looms?

Suggested preparatory steps

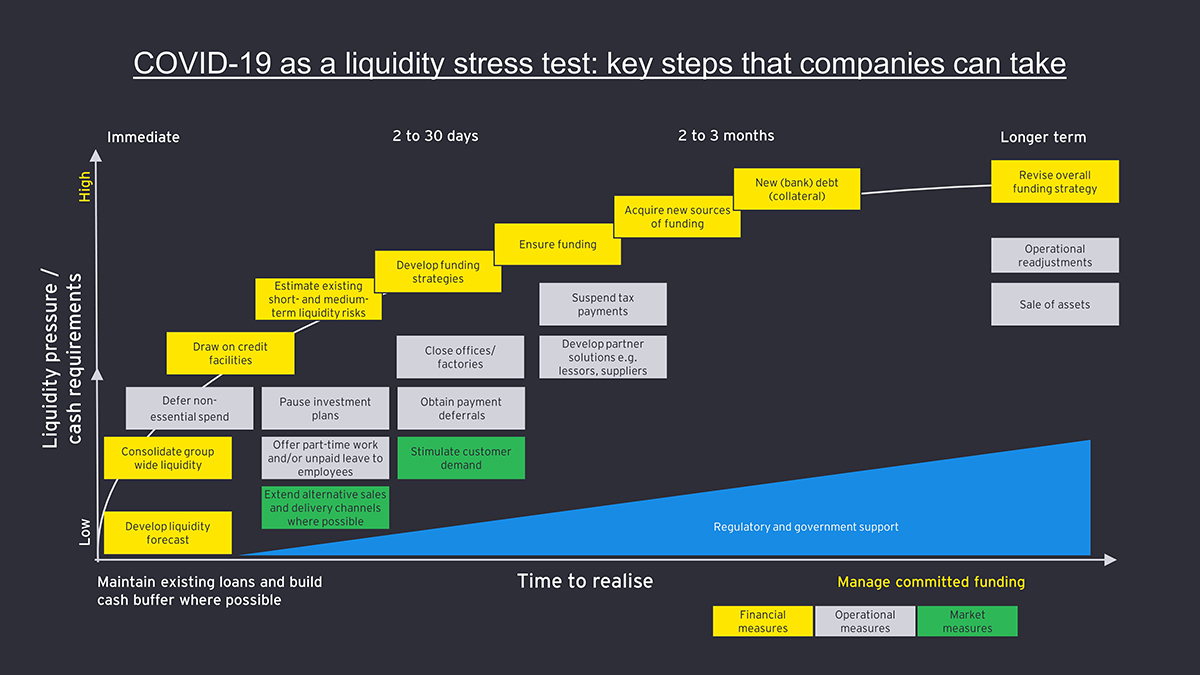

Stakeholders and companies can consider taking these steps (Figure 1) to navigate the current challenging times and potentially stave off a winding-up:

1) Focus on cash

To survive in the short term, companies should focus primarily on cash. This would involve closely managing liquidity using short-term cash flow forecasts to quantify short-term liquidity needs, evaluating sources to potentially free up cash, drawing on credit lines and realising near-liquid assets. Having visibility on a 13-week cash flow runway will assist companies in proactively managing imminent liquidity issues, which will in turn help maintain relationships with stakeholders including employees, suppliers, customers and financiers.

2) Consider an application for debt moratorium

Highly leveraged companies or companies in distressed sectors are likely to encounter challenging circumstances even after emerging from the temporary relief period of six months. These companies may consider availing themselves to the enhanced scheme of arrangement framework.

3) Early sourcing for white-knight investors, alternative capital providers, distressed funders

Continued access to new funds and raising capital may be critical for companies’ survival in the longer term. If traditional avenues of obtaining new financing may not be available, companies should explore alternative sources of funds early. For distressed companies, it is likely that financiers may require super priority status. This is available under the enhanced debt restructuring provisions.

Typically for family-run companies in Asia, one of the key concerns when considering bringing in new investors is the fear of “loss of control”. However, in a situation where the survival of a company is in question, delaying such a decision could result in severely destroying the company’s value.

Figure 1

CLOSING THOUGHTS

The new law reforms were introduced with the aim of offering rehabilitation and protection for companies, and facilitating restructurings. To further facilitate the ease of restructuring from a practical perspective, could a concession be made in relation to preparing the accounts and requirement for audit during the period of restructuring?

One of the key bases for preparing accounts is the going concern assumption. During the period of the moratorium, where a company is trying to restructure its debts, this will only be known with certainty when the scheme that is being proposed is approved by creditors and sanctioned by the Court. Could an automatic deferment to a specified number of months after the restructuring completion be considered? Could a similar concession to the reporting requirements under the Stock Exchange of Singapore Listing Manual Rules (Listing Manual) be considered for listed companies? It is encouraging that under IRDA (section 103), a company under judicial management is not required to comply with the requirements of holding annual general meetings and filing annual returns.

It is hoped that with the new provisions, including those that are currently not yet in force, local and foreign debtors seeking to restructure their indebtedness will avail themselves of the tools and techniques available under the new regime in Singapore at the earliest possible stages of stress and distress, in order to increase their chances of achieving a successful turnaround.

Angela Ee is the ASEAN and Singapore Restructuring Leader, Ernst & Young Solutions LLP. The views reflected in this article are the views of the author and do not necessarily reflect the views of the global EY organisation or its member firms.

This article was first published in ISCA Journal. You can read the original version here.

Related posts

August 5, 2025

July 9, 2024

{kind=link}

{kind=link}

{kind=link}