Biodiversity loss and ecosystem collapse are estimated to be under the top five risks to the global economy in the next 10 years. Almost 50% of global GDP, US$44 UDS, is moderately or highly dependent on nature.

which harm nature to those with nature-positive outcomes.

AUTHOR Thomas R van Viegen, Director, EARTH.INC.

“Nature is the next frontier in financial risk management.”

“Redirecting private finance and financial flows away from activities with a negative impact on biodiversity and ecosystem services towards those with nature positive outcomes.”

“Nature is no longer a corporate social responsibility issue, but a core and strategic risk management issue alongside climate change.”

An emerging nature thematic

The world has seen a rapid decline in biodiversity, predominantly driven by human activities to drive economic growth, which threatens the future viability of supporting natural ecosystems.

The Global Assessment Report on Biodiversity and Ecosystem Services states that ‘much of nature has already been lost, and what remains is continuing to decline”’. To date, 70% of land systems, 50% of freshwater, and 40% of oceans and seas have been significantly altered. Vertebrate populations have declined by 68% from 1970 levels, and two in five plants are estimated to be threatened with extinction. It is also projected that over half the world’s marine species will be near extinction by 2050. Global biomass and species abundance of wild fauna has fallen by 82% since the 1970s. Recent reports allude to the significant declines in arthropod and invertebrate biomass, and diversity, warning of a cascading collapse of global food systems.

Further, the World Bank estimates that the global economy could lose US$2.7 trillion by 2030 if ecosystems that support pollination, carbon storage, fisheries, and timber provision collapse. Global economic dependency on ecosystem services provided for free by nature are best illustrated by the pollination story. Currently US$235−577 billion worth of annual global food production relies on direct contributions by pollinators. However, pollination which allows for crop production continues to decline globally year-on-year, resulting in an estimated annual net loss of US$160−191 billion globally to crop consumers, and an additional loss of US$207−497 USD to value-added producers and secondary market value chain sectors.

A risk management framework for nature

There is growing evidence that this poses risks for businesses, capital providers, financial systems and economies, and that these risks are increasing in severity and frequency: nature-related risks and dependencies are material to business. Nature is the next frontier in financial risk management.

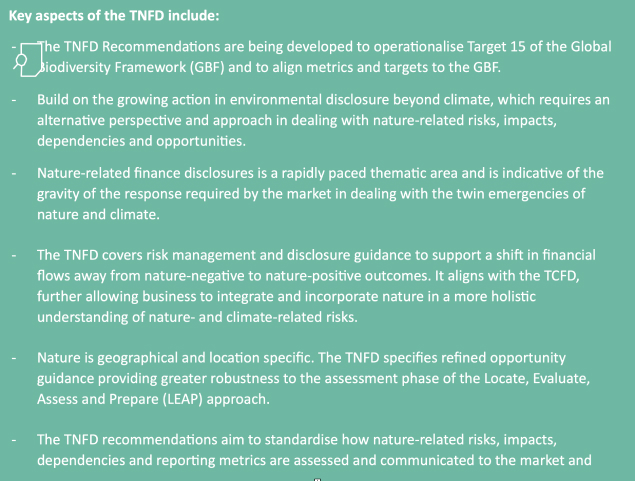

In response, the Task Force for Nature-related Financial Disclosure (TNFD) was established to encourage and facilitate a shift in corporate and business behaviour through enterprise and portfolio risk management and mainstream corporate reporting. The key objective of the TNFD framework is redirecting private finance and financial flows away from activities with a negative impact on biodiversity and ecosystem services towards those with nature positive outcomes.

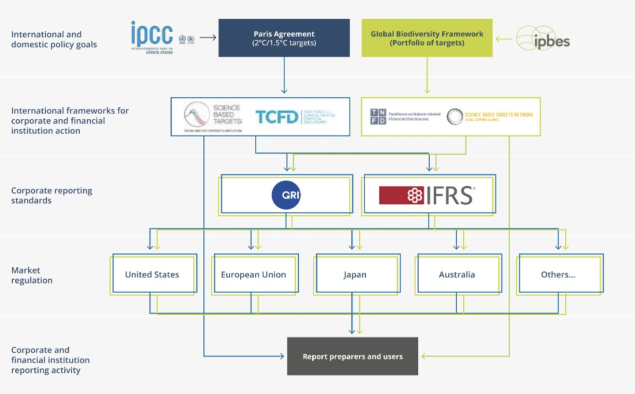

The TNFD was organised on the architecture of the Task Force on Climate-related Financial Disclosures (TCFD), building on the market’s experience with climate-related reporting over the past decade. The framework consists of a conceptual foundation for nature-related disclosures, a set of general requirements, and a set of recommended disclosures structured around four recommendation pillars − governance, strategy, risk and impact management, and metrics and targets. These are similarly consistent with, and build on, existing frameworks and standards, including those of the International Sustainability Standards Board (ISSB) IFRS Standards, and the Global Reporting Initiative (GRI).

Figure 1 Relationship between nature- and climate-related disclosure standards and frameworks

Source: TNFD While the TCFD is focused on a single metric of carbon dioxide equivalent (CO2e) to compare the emissions from respective greenhouse gases, nature is much more complex. What makes the TNFD framework unique is the ‘nature’ differentiator. To accommodate the complexity, diversity and variability of nature, the TNFD developed the ‘LEAP’ assessment approach to provide guidance to business in understanding the organisations location specific interphase with nature. Further, the LEAP process considers nature-related risks, impacts and dependencies; providing a calculated opportunity and scenario management response framework; and how to disclose on this information to stakeholders.

These recommendations provide companies and business of all sizes with a risk management and disclosure framework to identify, assess, manage and disclose nature-related issues.They have been designed to meet the corporate reporting requirements of organisations across jurisdictions, to be consistent with the global baseline for corporate sustainability reporting and to be aligned with the global policy goals in the Kunming-Montreal Global Biodiversity Framework.

A new deal for nature – the Global Biodiversity Framework

Nature and biodiversity, like climate change, are increasingly receiving greater attention and are being reassessed in the midst of this planetary emergency. The Global Assessment Report on Biodiversity and Ecosystem Services and subsequent studies highlighted the dire state of biodiversity loss, and the lack of current actions to address this enormous risk: a Global Deal for Nature (GDN) was therefore anticipated. Delays in the post 2020 CBD COP 15 due to Covid-19 and the poor performance in meeting the Aichi targets of COP 10 by 2020 intensified the need for global policy intervention to protect nature, and reverse current trends of nature loss. This global policy void placed significant expectations on the CBD COP 15, held in Montreal, Canada, in December 2022, and as a result the Global Biodiversity Framework was ratified by 196 countries. The GBF is considered the Paris Agreement for Nature and provides the underpinning global policy framework to lever support for nature positive outcomes.

The GBF incorporates a 2030 mission to ‘halt and reverse biodiversity loss’ and a 2050 vision for biodiversity to be ‘valued, conserved, restored and wisely used’. It provides a vision, mandate and framework for urgent and transformative action at the global and domestic level. Similar to the Paris Agreement, it is anticipated that the GBF will accelerate wide-ranging regulatory and policy reforms at a domestic level requisite to achieve the protected areas, limited chemical use, and government subsidies targets, amongst others.

The GBF is also seen as an important driver of national regulation on business and finance disclosure on nature. As countries update their National Biodiversity Strategy and Action Plans (NBSAPs), national regulations requiring business and finance disclosure on biodiversity and nature are likely to be introduced around the world. Understanding the critical importance that the capital markets play in redirecting finance towards nature positive outcomes, the GBF makes specific provision for the inclusion of the targets focused at business and financial policy mechanisms, namely targets 14 and 15. Target 15 is particularly pertinent to business. The TNFD framework as described above provides the segue for business to respond to emerging nature-related disclosure requirements.

Target 14 − Integrate Biodiversity in Decision-Making at Every Level

Provisions of Target 14 have direct implications for central banks and supervisors: Ensure the full integration of biodiversity and its multiple values into policies, regulations, planning and development processes, poverty eradication strategies, strategic environmental assessments, environmental impact assessments and, as appropriate, national accounting, within and across all levels of government and across all sectors, in particular those with significant impacts on biodiversity, progressively aligning all relevant public and private activities, fiscal and financial flows with the goals and targets of this framework (own emphasis).

This target will have implications for multiple organs of state who have a regulatory mandate over industry sectors, institutions and economic functions and activities. Including environmental authorities and finance system regulators and supervisors.

Target 15 − Businesses Assess, Disclose and Reduce Biodiversity-Related Risks and Negative Impacts

Target 15 has specific reference and implications for business and organisational behaviour:

Take legal, administrative or policy measures to encourage and enable businesses, and in particular to ensure that large and transnational companies and financial institutions […] regularly monitor, assess, and transparently disclose their risks, dependencies and impacts on biodiversity.

Aligning financial flows for nature positive outcomes

The Kunming-Montreal Global Biodiversity Framework (GBF) provides more concrete policy direction to protect and restore biodiversity and natural capital and it is now accepted that business has a key role to play.

The critical importance which business and particularly capital markets play in driving these broader impacts and corporate behaviours has only recently been understood. Activities which are primarily responsible for driving either positive or negative environmental change are all reliant on capital. The intention under the TNFD and the GBF is to now shift the flow of capital away from activities

{kind=link}

{kind=link}

{kind=link}