Audit and an Evolving Financial Reporting Ecosystem

Loading the Elevenlabs Text to Speech AudioNative Player...

By Jean Marc Mickeler and Shariq Barmaky

RELEVANT INFORMATION TO SERVE THE PUBLIC INTEREST

The debate about responsible reporting has not been sidelined by the Covid-19 pandemic. In fact, the future of audit, and how it should adapt to changing stakeholder demands, has only grown in importance as financial reporting ecosystem participants consider how to deliver reporting that provides insights for businesses and investors to recover and thrive.

To inform this debate, Deloitte Global surveyed 351 C-suite, finance and audit committee executives, investors, shareholders, and board members across nine countries from a broad spectrum of company sizes (revenues ranging from US$500 million to US$10 billion or more) in April and May 2020, to better understand the value they place on financial statement audits. The results show that even within the economic turmoil of the pandemic, market participants place great value on audits and the assurance that they provide.

In addition, the results unveil some of the most pressing Covid-19 concerns, many of which are still relevant today, as well as executives’ changing perceptions about the role of auditors in approaching these challenges.

AUDIT REMAINS ESSENTIAL

The survey results underscore the fact that audit is an integral part of the financial reporting ecosystem, providing one perspective on a business’s health. This ecosystem includes management, boards and those charged with governance, regulators, standard setters, auditors, and investors, with each having an important role to play.

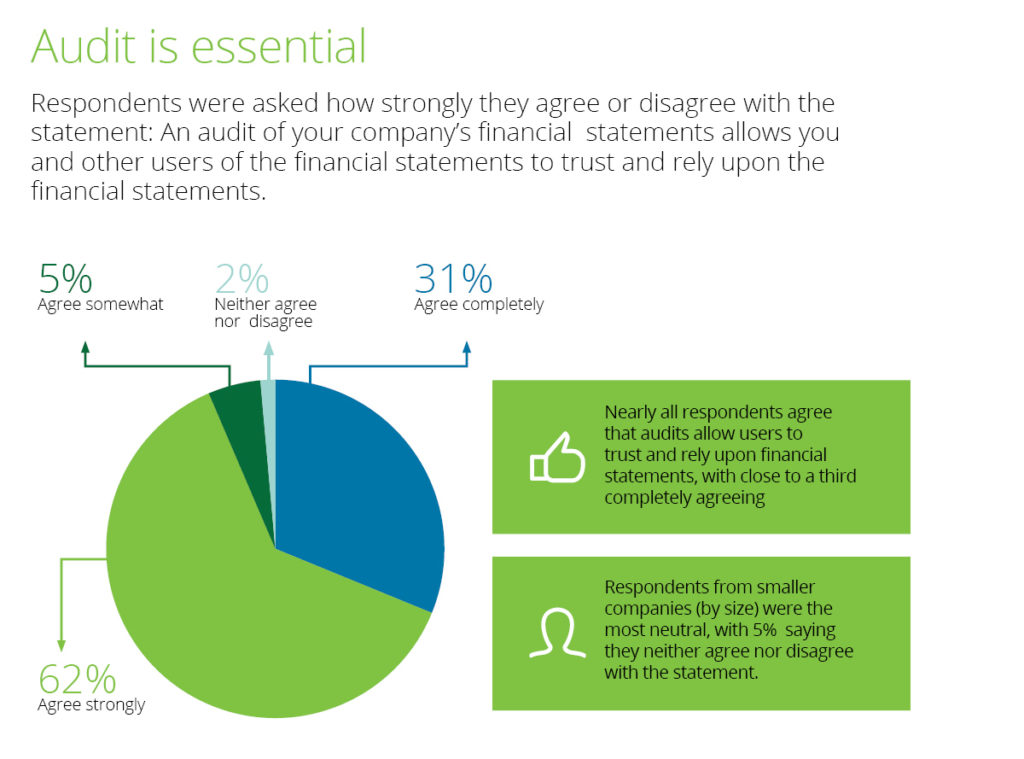

The survey respondents view audit as essential. Nearly all respondents agree that an audit of a company’s financial statements allows them to trust and rely on the financial statements.

Source: Deloitte Global Audit Value Pulse Survey 2020 Data Summary

Users of financial statements indicated that an audit enhances their confidence in a company’s financial information. However, there continues to be differing views about the perceived scope and purpose of audit. Today’s complex business environment requires the audit to be dynamic, multidimensional, and insightful in order to meet changing needs and expectations. Over the past few years, there has been a growing demand for audits to evolve and provide real-time, relevant information, and companies expect audits to keep pace as they innovate their businesses and processes.

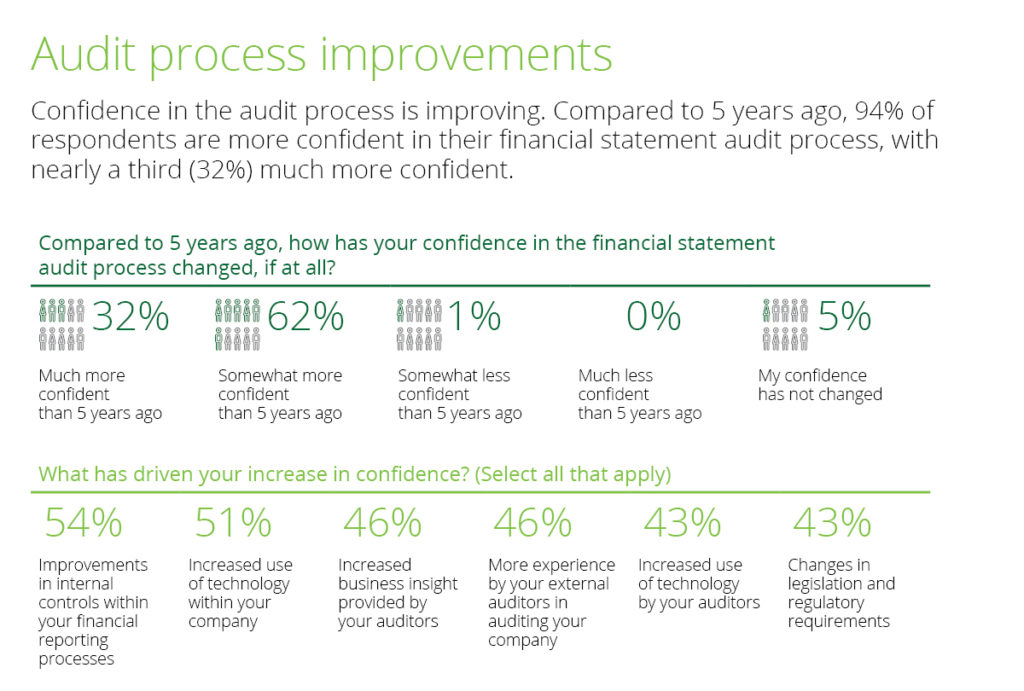

Many auditing firms are responding to these demands by investing in enhanced or new processes and technologies, and by equipping their audit professionals with the tools and knowledge to modernise the audit. These advancements seem to have made an impact, as 94% of respondents said that they are more confident in their financial statement audit process than they were five years ago, with nearly one-third (32%) answering that they are much more confident. Although great progress has been made, with increasing complexity, risk and expectations, there is more still to do.

Source: Deloitte Global Audit Value Pulse Survey 2020 Data Summary

EXPANDING AUDIT

The traditional approach to financial reporting – providing a historical view of financial information – has continued to come under scrutiny, as many would like to see it expand and include forward-looking elements that also cover a broader scope of topics.

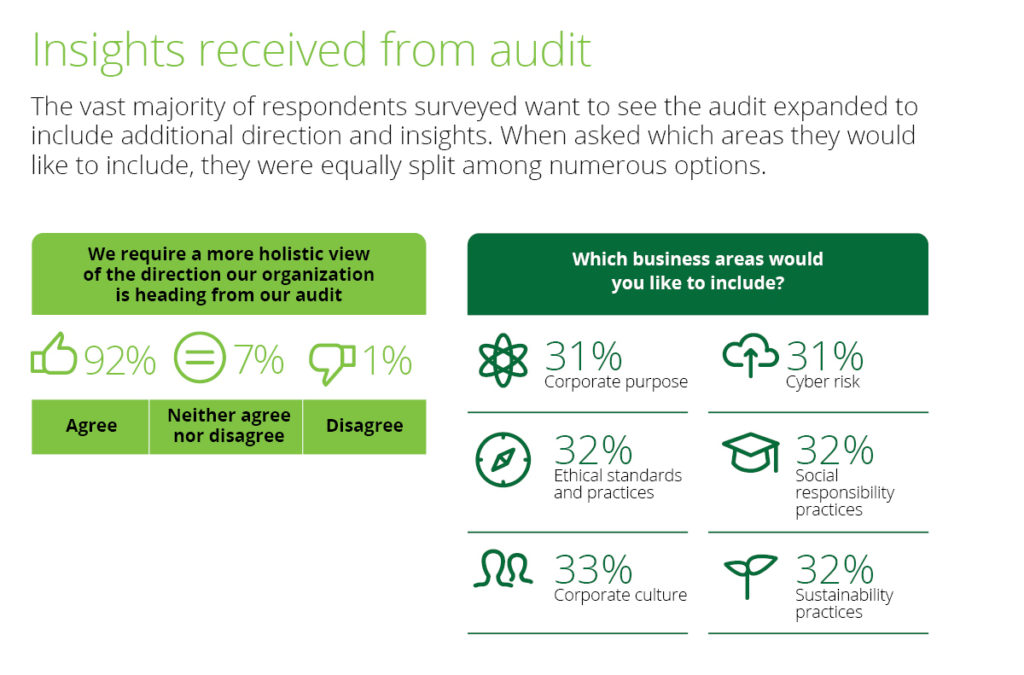

The survey polled respondents about the insights they would like to receive from their audits. Ninety-two per cent of respondents seek a more holistic view of the direction their organisation is heading from their audits. When asked which business areas beyond their financial statement audits they would like to include in the future, they were equally split among the following areas – corporate culture, sustainability practices, ethical standards and practices, social responsibility practices, corporate purpose, and cyber risk.

Source: Deloitte Global Audit Value Pulse Survey 2020 Data Summary

When asked specifically about financial statement audits, 95% of those surveyed said that a financial statement audit should provide additional value beyond providing an independent auditor’s report on the historical financial information. These findings suggest that there is a growing desire that a financial statement audit should inform as well as assure, extending its scope to areas of broader public interest and not solely historic financial statements.

Nearly three-quarters of respondents (73%) believe financial statement audits are designed to provide assurance that any fraud will be detected by the auditors, but the remaining 27% disagree. However, current professional standards and regulations require reasonable assurances rather than absolute assurances, indicating there are different expectations about what an audit is designed to do. The auditor’s responsibilities in relation to detecting fraud is an area of continued focus in adapting the scope of the audit and requires the constructive, integrated evolution of standards.

Fraud risk is not new, nor are the responsibilities of management and the board to have proper controls and processes in place to prevent and detect it, but recent corporate failures have increased focus on the topic, along with the responsibilities of the management, boards, regulators and auditors. The Covid-19 pandemic has resulted in significant operational and financial pressures on many companies and may have led to changes or weaknesses in their internal controls. As a result, audit firms are continuing to focus on the controls environment within the companies they audit, the messaging from leadership and tone at the top of those entities as well as exercising professional scepticism, ongoing assessment of risks, and the nature of audit evidence.

TRANSPARENCY EXPECTATIONS

Technological disruption, rapid market changes, and recent events have also highlighted the desire for greater transparency and breadth in reporting. A majority (65%) of executives surveyed cited the greater visibility and transparency around the process and outcomes of the audit as a way to address these expectations.

Further, there has been an increased focus on sustainability by a range of stakeholders. Over the past years, issues such as ESG (environmental, social and governance) performance have moved from being a fringe interest to a key factor in investment decisions.

Audit firms continue to actively engage with policymakers on the expanded scope of the audit. It is important to take a critical look at the auditor’s role within the financial reporting ecosystem and how more visible challenge and greater transparency can drive more meaningful financial reporting.

THE IMPORTANCE OF ASSESSING RISK

The survey reveals that respondents were seeking insights that could help them assess the risk presented by Covid-19 or similar disruptive events. In fact, 90% of executives felt that management could benefit by taking a page from the auditor’s playbook in assessing risks from such events. For example, adhering to sound internal control principles and practices, employing robust systems of quality control, and entrenching a culture of ethics and integrity can go a long way in helping an organisation remain resilient in times of crisis.

Businesses that seek to understand the long-term impacts of the crisis on their operating models are more likely to find new ways to quickly adapt to the post-Covid-19 world as well as use their experiences to prepare for future events.

ADDRESSING RESILIENCY CONCERNS

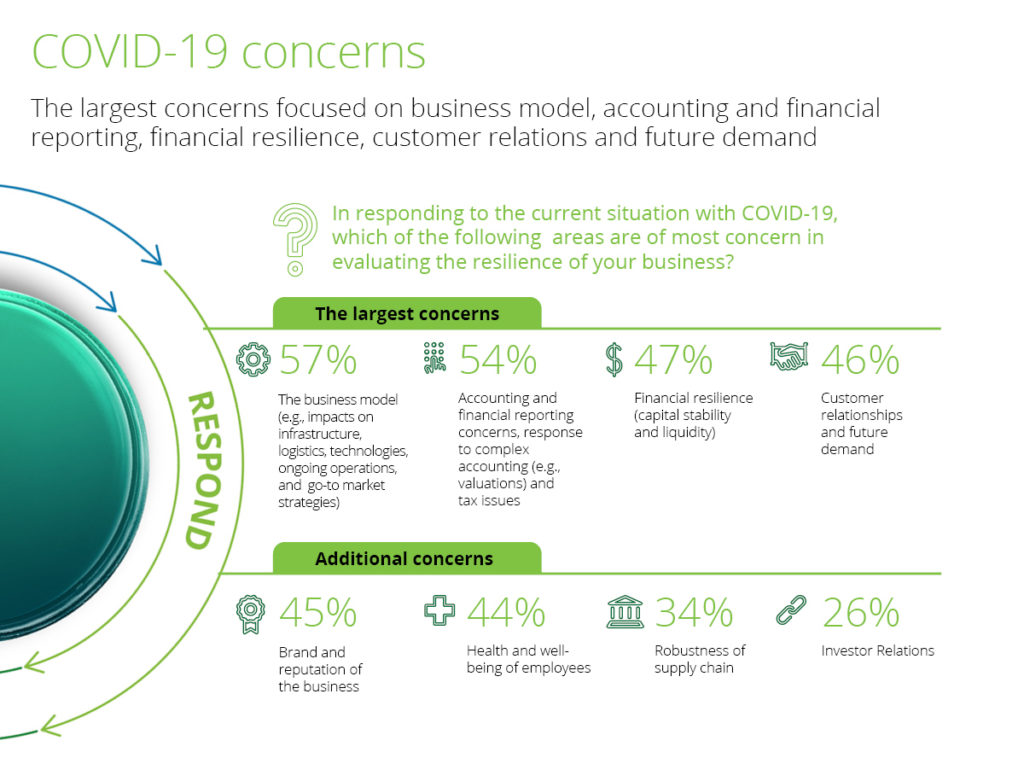

While the pandemic has exposed weaknesses in the ways some businesses operate, it has also ushered in a new reality of virtual working. This has created an even greater reliance on digital technology and collaboration tools, which is one of the factors leaving executives concerned about the long-term efficacy of their pre-Covid-19 business strategies. When asked about the resilience of their companies during Covid-19, the two largest concerns for respondents were viability of their business models (57%) and accounting and financial reporting issues (54%).

Source: Deloitte Global Audit Value COVID-19 Pulse Survey 2020 Data Summary

When viewed by geography, respondent concerns shifted somewhat. Brazil, France, India and the US rated business model concerns the highest. European respondents in general rated the health and well-being of their employees highest (49%), while Asia-Pacific respondents prioritised customer relationships and future demand (49%).

The pandemic has impacted industries in different ways and the results reflected these differences in executives’ concern by sector. For example, consumer products companies cited financial resilience (capital stability and liquidity) as their top concern (64%), while companies in the financial services industry were most concerned with the brand and reputation of their businesses (55%).

The economic and health crisis resulting from the pandemic has also caused the process of financial reporting to be far more challenging than before. Professionals must now deal with travel restrictions which prevent routine in-person meetings and activities, market volatility that impacts estimates and valuations, challenges of cross-border data sharing, and complex tax implications of work-from-home mandates. It is therefore unsurprising that 54% of executives shared that navigating accounting and financial reporting issues was a top concern – this was an especially common concern among investors. They are seeking objective insights into systems of control and quality that inform guidance in difficult decisions relating to forecasts, estimates, and other judgements related to valuations and complex accounting treatments.

When asked what actions their businesses were planning to take to respond to Covid-19 challenges, 63% of executives said they were focusing on communications with investors and stakeholders on business challenges and impacts. This response amplifies the positive potential impact that constructive engagement throughout the financial reporting ecosystem could have on markets.

Many regulators have acknowledged the uncertainties created by Covid-19 and emphasised the need for high-quality reporting that includes the transparent disclosure of new risks and assumptions made. These comments have provided some assurance for reporters and users of financial statements alike, and more regulator input could go a long way in reinforcing trust and reliability.

Access to timely, transparent, meaningful data and insights to inform financial reporting and associated disclosures remains critical. It enables stakeholders – investors, employees, suppliers, governments, and regulators – to identify which companies have so far mitigated the disruptive effects of the pandemic.

A FINANCIAL REPORTING ECOSYSTEM FIT FOR THE FUTURE

As expectations evolve, it is clear that the entire financial reporting ecosystem will need to continue to adapt as an integrated whole. All players across the ecosystem have a collective responsibility to serve the public interest. More forward-looking reporting, covering both financial and non-financial matters such as climate and ethics, is an important step in this evolution. Ultimately, any changes implemented need to drive responsible business behaviours, improve clarity and transparency of relevant reporting, and provide stakeholders with more meaningful information to equip them to make informed decisions.

The auditor is critical, but only one part of the financial reporting ecosystem – continued constructive collaboration – is needed to drive further change. Audit firms have a significant opportunity and responsibility to drive more value-added reporting and continue to challenge ourselves on how we can adapt for the future.

Jean-Marc Mickeler is Deloitte Global Audit & Assurance Business Leader, and Shariq Barmaky is Deloitte Southeast Asia Audit & Assurance Regional Managing Partner. For queries on the survey, contact Deloitte Global Audit & Assurance Brand, Communications & Marketing or Deloitte Southeast Asia Enquiries.

This article was first published by ISCA Journal. You can visit the original page here.

{kind=link}

{kind=link}

{kind=link}